Discover why homes near a university can be a smart choice for homebuyers. Learn how strong local employment, steady housing demand, and community amenities can support long term value while making an informed homebuying decision.

Published on 08/03/2026

Should you sell your current home before buying your next one? Learn the pros, cons, financing options, and key factors that can help you make the best move for your financial situation.

Published on 07/27/2026

Learn the difference between hazard insurance and homeowners insurance, what lenders require, what each policy covers, and how understanding both helps prevent closing day surprises.

Published on 07/20/2026

Virginia’s housing inventory is improving overall, but Richmond-area buyers are still navigating a tight, competitive market. Here’s what the latest statewide and local data—along with mortgage rates averaging in the mid-6% range—means for your home search, budget, and financing strategy.

Published on 07/17/2026

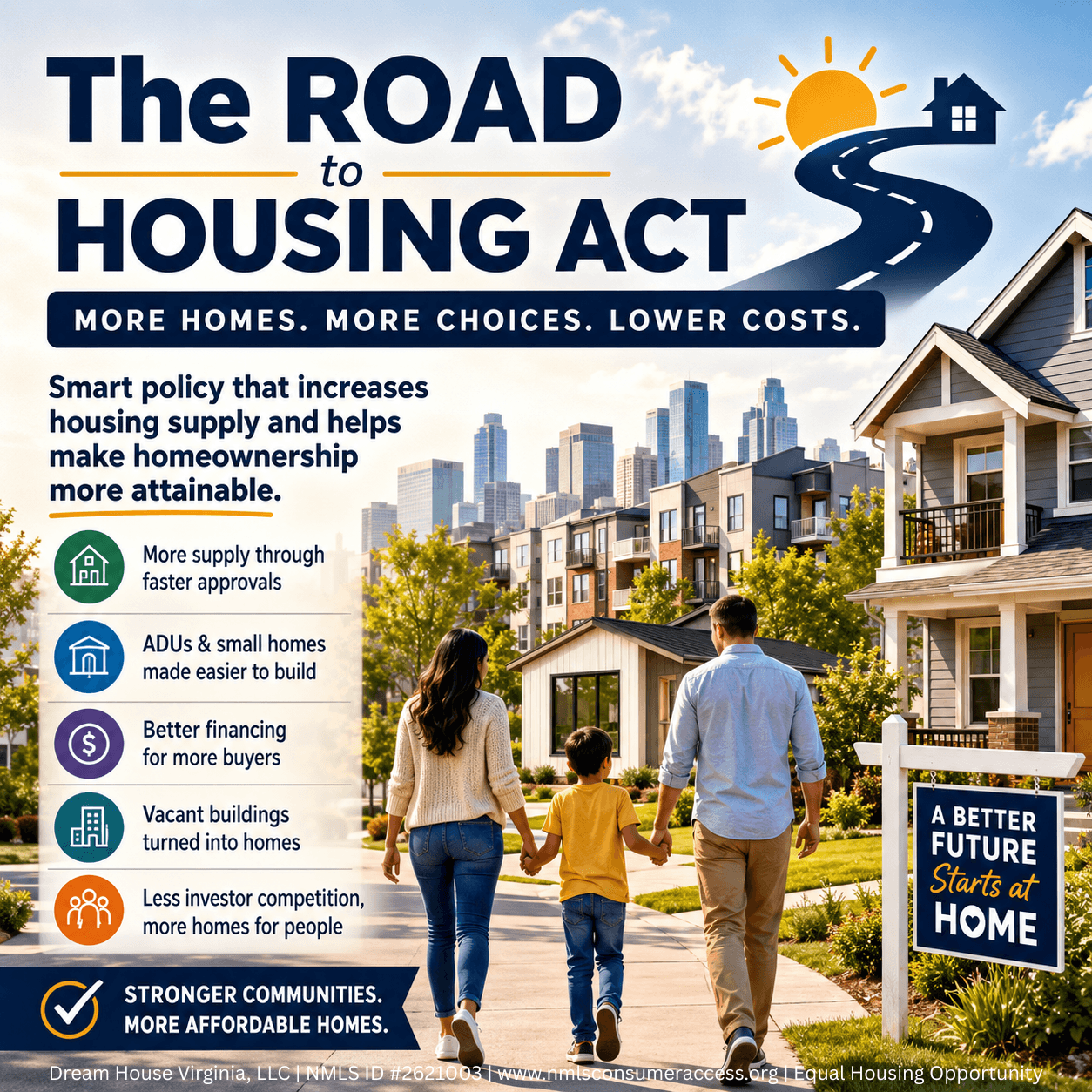

The ROAD to Housing Act will not lower prices overnight, but it targets several real cost drivers: local permitting delays, ADU approvals, manufactured housing rules, small-dollar mortgage access, adaptive reuse, affordable housing funding, and large institutional investor activity.

Published on 06/26/2026

The Fed held rates steady, but that does not mean mortgage rates stop moving. Inflation still plays a major role in where mortgage rates go, which is why buyers should focus less on the headline and more on their actual payment, loan options, and updated pre-approval numbers.

Published on 06/23/2026

Homebuying tips FSBO

Published on 06/22/2026