An old pre-approval may not reflect today’s rates, payment, taxes, insurance, or buyer comfort level. Before writing an offer, buyers should refresh their numbers so they can move forward with confidence.

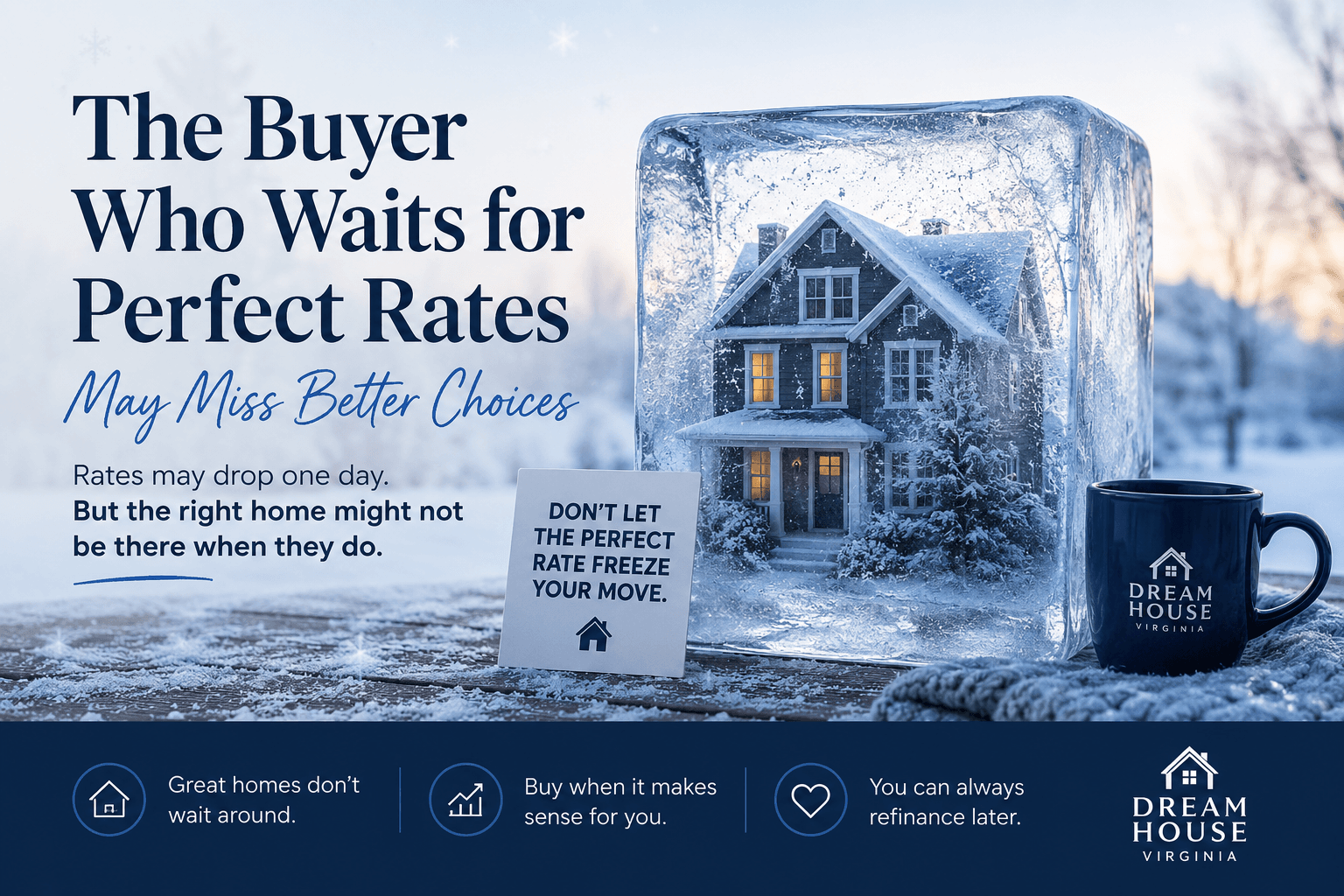

Many buyers are waiting for better mortgage rates, but waiting for perfect conditions can come with tradeoffs. Better inventory, seller flexibility, and negotiating room may matter just as much as the rate itself.

Before a seller drops the price, it may be worth looking at the full deal structure. In some cases, seller credits can help buyers more directly than a price cut by reducing cash-to-close pressure, supporting payment strategy, or creating room for a rate buydown.

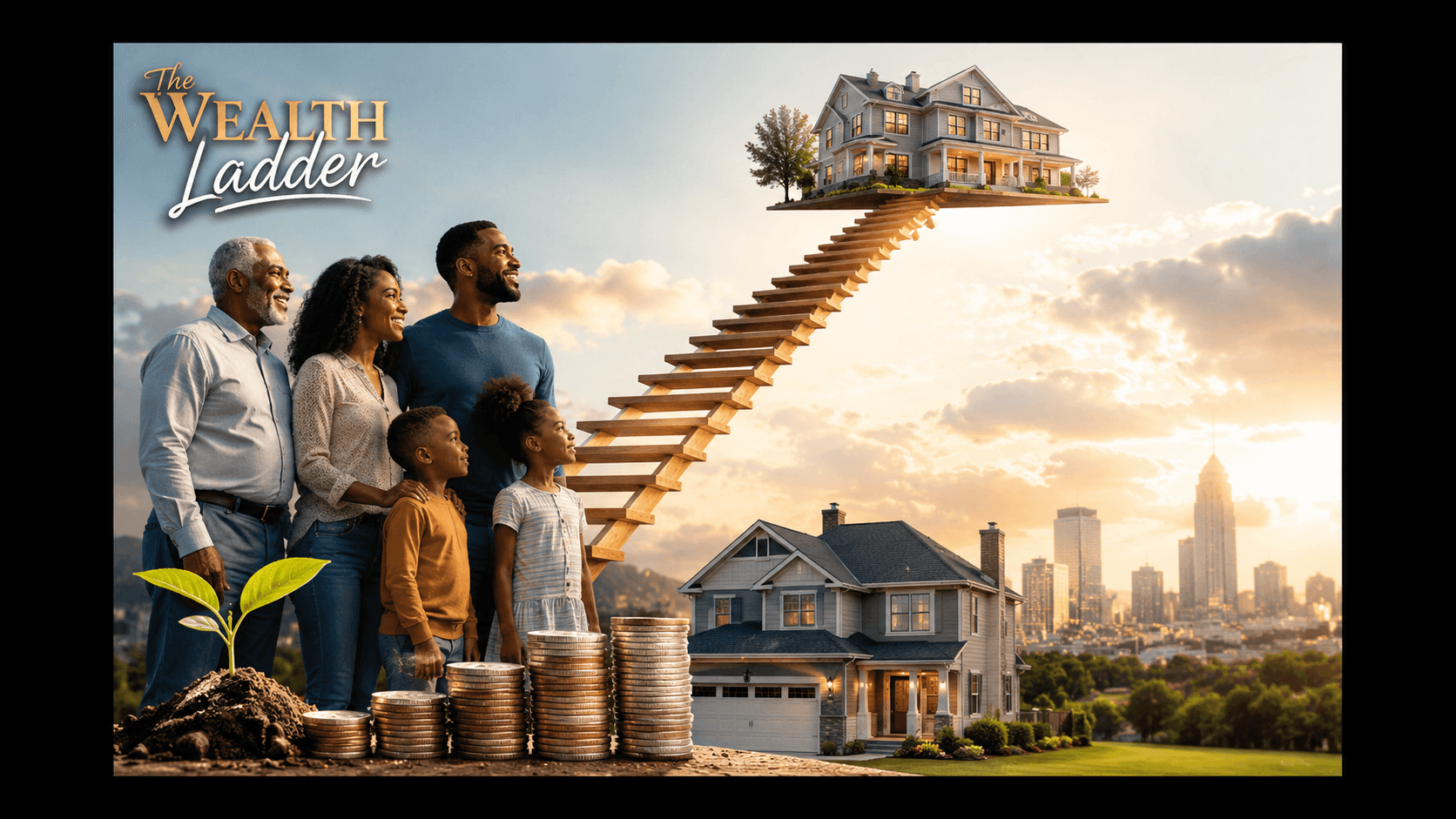

Homeownership builds wealth

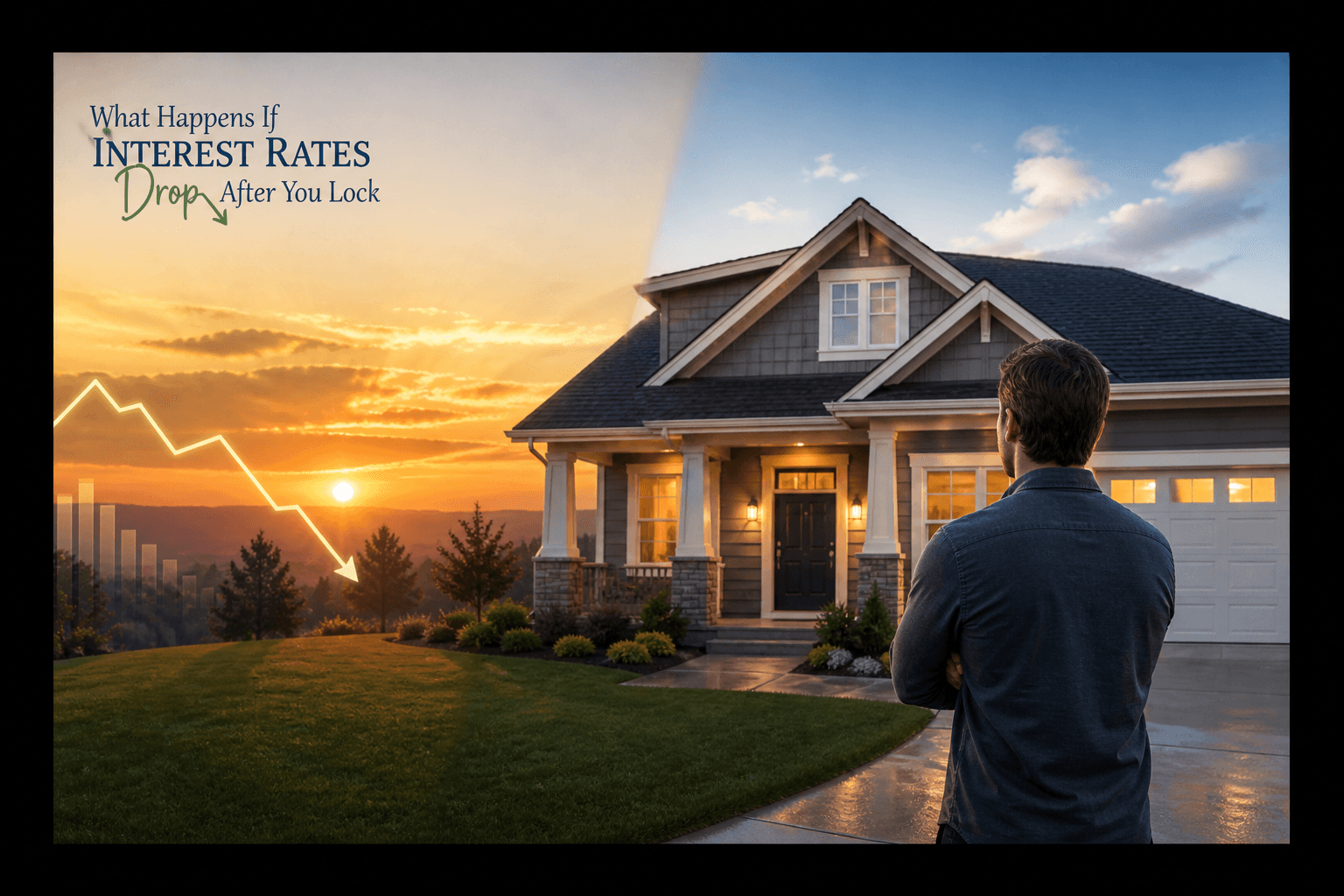

What to do if rates drop after you locked your rate?

More homes on the market can give buyers more options, but it does not automatically fix affordability. With rates, insurance, taxes, and monthly payments still weighing heavily, today’s buyers need updated numbers, realistic payment expectations, and a strategy that looks beyond the list price.

An old pre-approval can give buyers a false sense of confidence. Rates, payments, credit balances, cash to close, and property details can all change, so it is important to refresh your numbers before touring seriously or writing an offer.

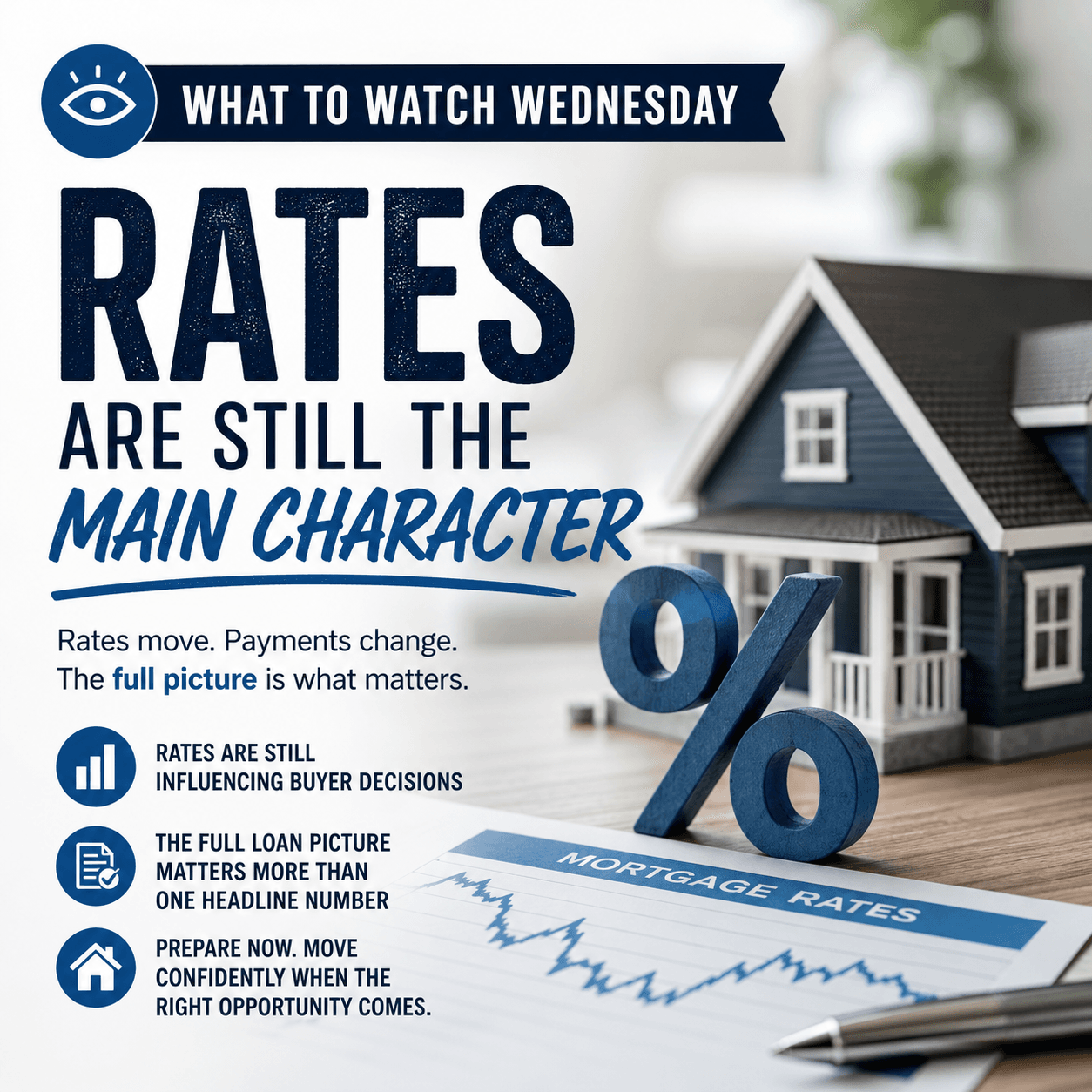

Mortgage rates are still driving the housing conversation, but they are not the whole story. Here is what buyers and realtors should watch right now, from payment impact to pre-approval quality, and why understanding the full loan picture matters more than chasing one headline number.

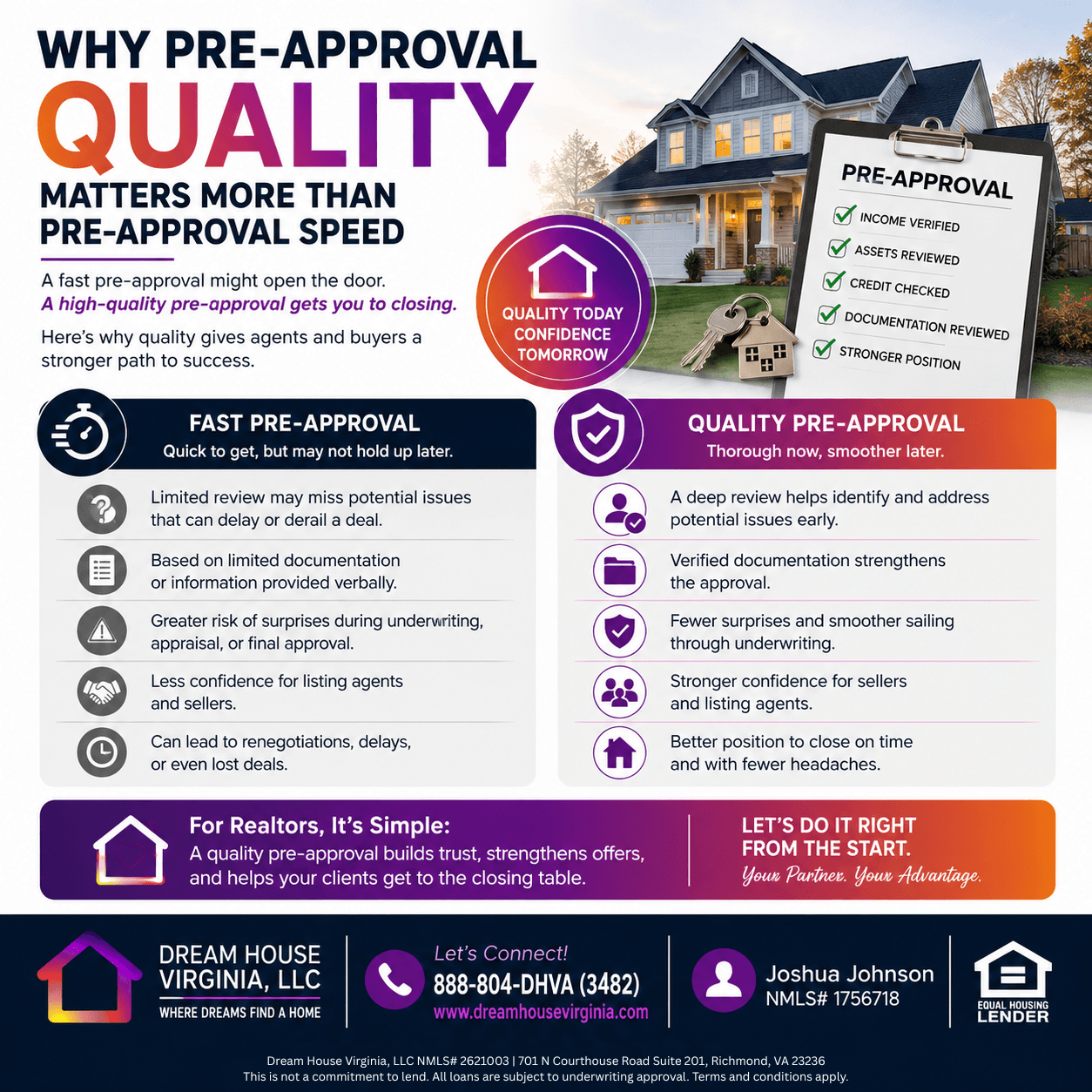

A fast pre-approval might look impressive, but a high-quality pre-approval is what really helps deals hold together. This post explains why a thorough review of income, assets, credit, and documentation gives realtors and buyers a stronger path to closing than speed alone.